Empirical research has found that at moderate levels debt can improve growth, but at high levels (thresholds somewhere between 75% and 100%) it can become harmful (if the high ratio is not addressed and becomes persistent) – debt becomes drag on economic growth. (See the 2011 study “The real effects of debt“2013 study”Does high public debt constantly hinder economic growth?” study of 2020″Debt and Growth: A Decade of Studies” and the studies of 2021″The Impact of Public Debt on Economic Growth“and”Public Debt and Economic Growth: Panel Data Evidence for Asian Countries.”)

Explanations for the negative economic impact include: higher interest rates (investors, especially foreign investors, may demand a higher risk premium), higher taxes (which reduce income), constraints on future ability to provide countercyclical fiscal policy to combat recessions (leading to greater economic instability), withdrawal of private sector investment (reducing innovation and productivity), and increased interest payments that consume an increasing portion of the federal budget, leaving more small amounts of public investment in research and development, infrastructure and education.

Congressional Budget Office (an independent agency created in 1974) ASSESSMENTthe US debt-to-GDP ratio stands at 98% at the end of 2023 and is projected to reach 181% in 30 years. With these predictions in mind, Roberto Cram, Howard Kung and Hanno Lustig, authors of the September 2023 study “Can US Treasury markets add and subtract?,” analyzed all (15,533) CBO cost releases for all bills introduced by Congress from 1997 to 2022. Their objective was to determine the impact of spending increases on interest rates. Below is a summary of their key findings:

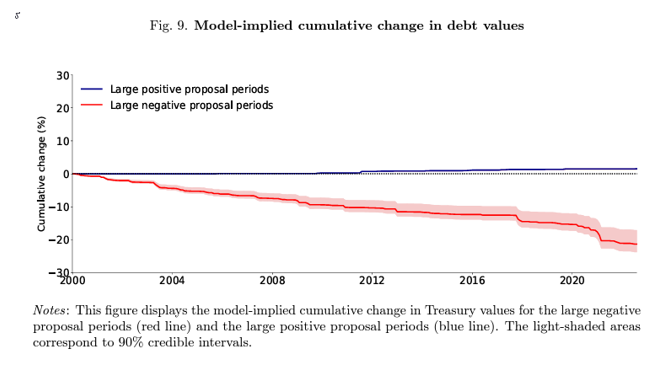

- Cost releases with large negative cash flow projections have reduced the valuation of all Treasuries outstanding by more than 20% between 1997 and 2022. Cost releases allowed investors to learn about the downside move in surplus policy. Large negative cost releases generated significant revisions in expectations, leading to systematic negative treasury value responses.

According to John Cochrane Fiscal theory of the price levelmarket expectations for inflation also increased across horizons in the daily event windows around large days of negative proposals, especially over long horizons.

The Treasury valuation effects of negative fiscal news were concentrated at longer maturities, with an overall 4% increase in long-term nominal yields. The increase was driven by an increase in long-term premiums and inflationary expectations and by a decline in the effective yield (the value investors assign to the liquidity and safety attributes) of Treasury securities.

The authors noted: “During their sample period, Fed policy imposed a downward secular shift in long-term bond yields. Over the same sample period, the cumulative change in the 10-year nominal yield on FOMC meeting days is -3.18%. FOMC announcements effectively offset the entire effect of cost releases.

Their findings led the authors to conclude: “In daily event windows, we find that cost releases of large proposals expected to increase future deficits significantly lower Treasury estimates.”

Using their estimated model, they conclude that a surprising 1 percentage point increase in the Treasury supply, expressed as a share of GDP, corresponds to a 31 basis point increase in the 10-year nominal yield basis and a drop in the comfortable yield of 7.5 basis points. With CBO estimating that there would be an 83 percentage point increase (from 98% to 181%) in the debt-to-GDP ratio, there would be a dramatic increase in the cost of government debt with a negative impact on so dramatic in the economy. growth.

Investor Takeaway

CBO's cost projections of future deficits contain valuable budget news, allowing bond investors to learn about the trajectory of the debt-to-GDP ratio. The takeaway for investors is that their financial plans should take into account a possible negative impact on economic growth caused by increased debt and that this could lead to lower returns on capital. The lowest possible economic growth along with the risk of rising inflation, when combined with historically high valuations of US stocks, as represented by the S&P 500, should at least raise concerns. Prudent investors plan for these risks. For example, they adjust forecasts of future returns to reflect current valuations and yields (as opposed to relying on historical returns). They may also consider increasing allocations to fixed-income assets that are less sensitive to inflation shocks (such as TIPS and floating-rate debt) and raising discount rates for Treasuries. They may also consider increasing exposure to risk assets that are less correlated to economic growth and inflation risks – such as reinsurance (using gap funds such as SRRIX AND XILSX) and short factor strategies (such as AQRs). QSPRX AND QRPRX).

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners, collectively Buckingham Strategic Wealth, LLC and Buckingham Strategic Partners, LLC.

For informational and educational purposes and should not be construed as specific investment, accounting, legal or tax advice. Some information is based on data from third parties and may become out of date or be replaced without notice. Third-party information is believed to be reliable, but its accuracy and completeness cannot be guaranteed. The opinions expressed herein are their own and may not accurately reflect those of Buckingham Strategic Wealth, LLC or Buckingham Strategic Partners, LLC, collectively Buckingham Wealth Partners. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article. LSR-23-617